Monthly Tax Update – July 2015

6 July 2015

Welcome to our monthly tax update designed to keep you informed of the latest tax issues.

In this issue we focus on issues to be considered before the end of the tax year and things to look forward to next year. As ever we are here to help you so please contact us if you need further information.

The Dog ate my tax return

The Dog ate my tax return

… is not a reasonable excuse!

However, it has been announced that HMRC will not contest appeals against the £100 late filing penalty in respect of 2013/14 tax returns where the taxpayer provided a reasonable excuse for not filing on time.

In the past, HMRC has looked in detail to judge if each excuse is reasonable but will now reallocate resources onto tax evasion and avoidance.

What counts as a reasonable excuse is normally something unexpected or outside your control that stopped you meeting a tax obligation, for example:

- Death of your partner shortly before the deadline

- An unexpected stay in hospital

- Your computer or software failed just before or while you were preparing your return online

- HMRC online service issues

- Postal delays that couldn’t be predicted

Although the latest announcement concerns late self-assessment tax returns, the above list of excuses applies generally to other returns and payments such as VAT, PAYE and those due under the Construction Industry Scheme.

Inheritance tax and the family home

Further detail has emerged (in a leak to the Guardian newspaper) concerning a new Inheritance Tax (IHT) allowance announced in the Conservative Party election manifesto to set against the value of the family home.

The proposed new family home allowance provides for an additional £175,000 nil rate band from April 2017, bringing a couple’s combined tax free estate to £1,000,000. This allowance is subject to a taper where the amount being left is more than £2,000,000 with £1 of the family home allowance being lost for every £2 of estate value over £2,000,000. This clawback seems to be based on the value of the estate before reliefs such as business property relief and agricultural property relief and may result in some additional complications and redrafting of Wills.

We will almost certainly see further details announced in the Summer Budget on 8th July and you may wish to arrange a meeting with us to consider the impact on your Will and your family’s inheritance tax position.

Relief for political gifts

The General Election result means that donations to the UK Independence Party now qualify for relief from inheritance tax as that party returned at least one member and secured at least 150,000 votes nationally. However, the Alliance Party in Northern Ireland now ceases to qualify.

Remember that this relief applies to gifts during the donor’s lifetime as well as bequests made to a qualifying party in their Will.

These donations need to be made personally, as such payments are not an allowable deduction in arriving at business profits.

Shares to employees and directors

Whenever companies issue shares to employees and directors, they need to consider whether or not an entry needs to be made on the end of year HMRC Form 42. This form is used to report events relating to shares and securities obtained by reason of employment and now needs to be submitted online by 6th July following the end of the tax year.

Remember that where the shares are issued at an undervalue there is potentially a charge to employment income. Note that there are a number of exceptions from the need to make a report and that different forms are used to report shares acquired under tax-advantaged schemes such as EMI share options which we referred to last month.

The main exceptions from the reporting obligation are where shares are issued in connection with incorporation and where there is a transfer of shares in the normal course of the domestic, family or personal relationships. An example of the latter would be the gift of shares from father to son or daughter as part of an estate planning exercise. However, HMRC guidance states that there must be no element of remuneration in the award or grant. Please contact us for assistance whenever you are considering the transfer of shares to family members or other employees.

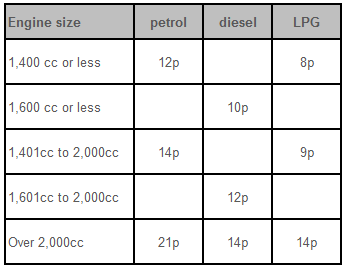

Company car advisory fuel rates

These rates are the suggested reimbursement rates for employees’ private mileage in their company cars and are reviewed each quarter on 1 March, 1 June, 1 September and 1 December. In line with an increase in fuel prices, the rates that apply from 1 June 2015 are as follows:

Tax diary of main events for July/August 2015

1 July – Corporation tax for year to 30/9/14

1 July – Corporation tax for year to 30/9/14

6 July – Forms P11D and P11D(b) for 2014/15 tax year, and where appropriate form P9D

6 July – Form 42 – shares issued to employees (see earlier)

19 July – PAYE & NIC deductions, and CIS return and tax, for month to 5/7/15 (due 22 July if you pay electronically); payment of Class 1A NICs for 2014/15 (22 July if you pay electronically)

31 July – Second 50% payment on account of self-assessment income tax for 2014/15

1 August – Corporation tax for year to 31/10/14

19 August – PAYE & NIC deductions, and CIS return and tax, for month to 5/8/15 (due 22 June if you pay electronically)

- Financial Support for Businesses during Coronavirus (COVID-19) - 21 April 2020

- Coronavirus Update – 2 April 2020 - 2 April 2020

- Entrepreneurs’ relief lifetime limit slashed from £10m to £1m - 2 April 2020

- Chancellor ups annual pension allowance thresholds by £90,000 - 2 April 2020

- Coronavirus pandemic prompts one-year business rates holiday - 2 April 2020